Pining For Better Stumpage Prices

- Tim Cartner, RF

- Oct 30, 2020

- 8 min read

Updated: Apr 9

"Your business must be booming?" "I bet timber prices are really good, eh?" I hear these remarks quite frequently these days. The pandemic building spree has pushed lumber prices to historic highs. Consumers see and feel the increase every time they go to the local lumber store or get a quote for a construction project. Unfortunately for timber growers, the increase in lumber prices has not translated into a windfall. As a matter of fact, except for outlier cases, the value of standing pine timber (stumpage value) has changed very little.

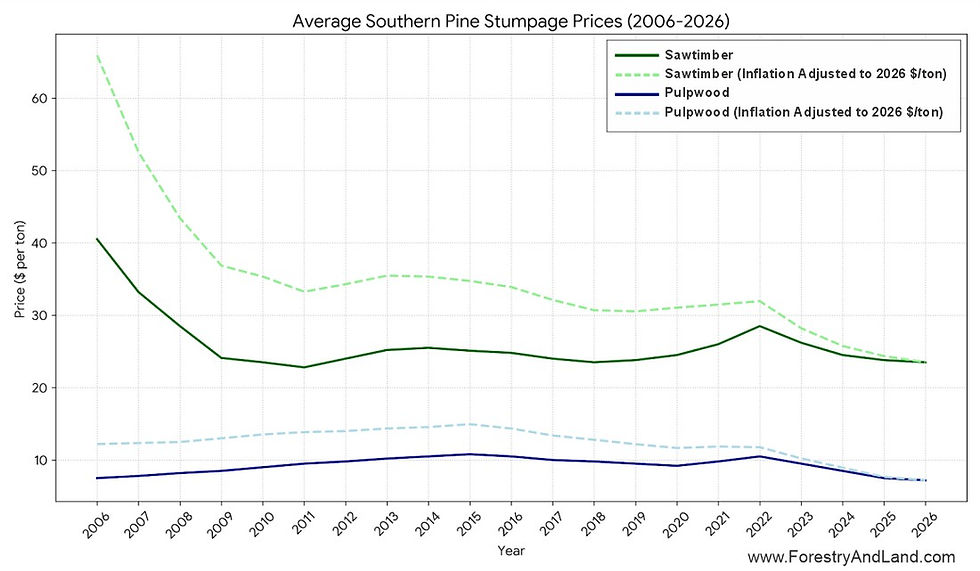

Since the onset of the Great Recession, pine chip-n-saw and sawtimber prices have dropped and have stayed relatively stagnate. The graph below shows the average pine chip-n-saw and sawtimber stumpage prices for the Southeast since before the Great Recession.

See current TMS South-wide averages here.

The graph above doesn't tell the whole story—there is no adjustment for inflation. Using the Bureau of Labor Statistics inflation calculator, I've computed that the average of $40.00 per ton my clients were getting for pine sawtimber before the Great Recession is equivalent to $51.43 per ton in today's money. Depending on where you are in the Carolinas, the current regional average pine sawtimber price ranges from ±$19 per ton to ±$27 per ton, averaging ±$22 per ton overall. This sawtimber price average is less half of what it once was in real dollar terms. Furthermore, mills have tightened their specifications, meaning that $22 per ton buys them a higher quality product than the $40 per ton did back in pre-Great Recession times.

Reasons for Mediocre Pine Sawtimber Stumpage Prices

Government incentive programs (Conservation Reserve Program, Forest Development Program, Etc.) have encouraged and incentivized planting trees (mainly pine) for decades. These programs have created a glut of stumpage supply, negatively distorting the market supply and demand balance. The Wall Street Journal addressed this issue in an October 2019 article.

A declining number of mills in the Southeast. While we are back to prerecession production levels, fewer, larger mills are meeting the demand. Throughout my career (starting in 1994), there has been a steady reduction in the number of mills, meaning fewer producers have more control over stumpage prices. A research paper published in the August 2015 edition of Forest Science predicts this trend to continue. Large mills have greater efficiency through economies of scale and can more readily deal with liability issues.

Sawmill production is not at a level that outpaces pine volume growth and the logging forces' ability to supply them with raw materials. For those of you of a certain age, think of Lucy and Ethel working in the chocolate factory, and you'll have a pretty good visual of the pine supply situation.

The home building surges of the 1990s and early 2000s resulted in lots of clearcut harvesting. These harvests were followed by reforestation with pine (much of which was subsidized and incentivized by Uncle Sam).

When the Great Recession hit, pine sawtimber prices fell. Most landowners held off on clearcut harvesting, thinning stands instead, waiting for sawtimber prices to rise. That rise never materialized, and the trees kept growing over the decade-long economic malaise, adding to the standing sawtimber inventory.

Improved pine genetics grow more tons per acre in less time.

Will Pine Sawtimber Stumpage Prices Recover to Pre-Great Recession Levels?

I'm not optimistic that they will, at least not in the near future. I can't think of any reason prices will rise, except for brief spikes caused by extreme weather situations that cause mill inventories to dip dangerously low.

Factors I see working against a price increase:

Pine volumes will increase over the next decade in most southern states. Even if volumes aren't rising in your area, the mills local to you will have to compete with the lumber prices from the regions flush with inventory, keeping overall stumpage prices down.

Much of our younger generations are burdened with college debt. I speculate that even if they do ever get around to building houses in large numbers, they'll be much less grandiose than those of the Boomers and Gen-Xers, utilizing fewer forest products.

Logging costs are rising (equipment, liability insurance, workers' compensation insurance, labor). These costs come directly out of the stumpage price (the price paid to the landowner for standing timber) equation: Delivered Mill Price – Logging and Transport Costs – Buyer Profit = Stumpage Price

Replacement Products. Less large diameter wood is needed for construction these days. Oriented strand board (OSB), made mostly from flaked pulpwood, has mostly replaced plywood, which is made from larger, more expensive "peeler logs." Engineered I-beams (made mainly from OSB) are now used for floor joists instead of large diameter lumber. Most 2x4 wall studs come from northern softwoods. Additionally, engineered strand-board 2x4s are now being produced and will most likely gain market share over time as technology improves and production costs decline. They are a superior product (perfectly straight, no warping) to a plantation-grown 2x4.

Each new economic slowdown we have will exacerbate the supply problem—trees won't stop growing just because the economy does.

Worldwide, plantation forest acreage is increasing. From 1990 to 2015, planted forest areas increased from 414 million acres to 687 million acres. So not only are we dealing with Southern plantation volumes, we'll be competing with global plantations. Simplistic green schemes to capture carbon such as the One Trillion Trees Initiative could further depress stumpage prices.

The government is still paying people to plant pine trees. While I'm sure the various government agencies administering these programs think they are "helping" landowners, what they are doing is throwing fuel on the fire, adding to the bloated future volumes. The subsidies you'll get from the government for reforestation are a pittance compared to the damage they do to the future value of your timber. In addition to negatively distorting stumpage prices, subsides also incentivize replacing biodiverse native forests' with single-species loblolly plantations.

It's not that pine mills can't pay more; they don't have to. An example of this ability to pay more occurred in 2018. That summer, southern yellow pine lumber prices hit an all-time high (September 2020 lumber prices almost doubled the 2018 mark). Even so, stumpage prices didn't budge because the mills' wood yards were full. In December 2018, lumber prices had declined, but excessive rain curtailed logging to the point that some mills were close to running out of logs to process. Mills responded by paying prerecession stumpage prices for timber on tracts loggable in wet-weather conditions (high-ground, well-drained, roadside access). During this log shortage, I placed a client's wet-weather pine tract (28 acres of loblolly pine) on the market for bids. The pine timber on the tract was of a good size but of mediocre quality. Under normal weather conditions, the timber would've brought around $90,000. We received six bids, ranging from a low of $84,484 to a high bid of $145,600 (average bid was $114,512). Based on my volume estimations, the high-bidder placed at least $40 per ton on the pine sawtimber to have arrived at that bid price. Within a couple of months, the log shortage was over, even though the rains continued. The logging force had moved to high ground, and the mills were full of logs again. Dry weather was just around the corner. High bid prices ceased.

Timberland Investment and Management Strategies Going Forward

Diversify. If you have areas that will regenerate in desirable hardwood following a harvest, allow some of them to do so. You wouldn't invest all of your retirement in one stock, so don't put all of your timber investment in one species. A diverse species base is not only better for the environment as a whole but will also reduce your risk level from losses from down markets, insects, and disease. If climate change is a concern for you, diverse natural forests are more reliable vessels for absorbing and storing carbon over time than monoculture plantations.

Unless you own timberland in an area where pulpwood demand and price are high, and you are strictly managing pulpwood rotations, plant your pines at a wider spacing (300 to 436 trees per acre). The wider-spaced planting will cost less upfront and delay the first thinning a few years beyond a more traditional spacing (550+ trees per acre). When the stand is ready for its first thinning harvest, it'll have taller, healthier, larger diameter trees with a blend of pulpwood, chip-n-saw, and sawtimber rather than just pulpwood. Low-density plantings also have other advantages; read more about planting density options here.

Don't take your harvest scheduling and management advice from government agents, or at the very least, get a second opinion from someone on the private side of the forestry profession for a realistic picture of costs, benefits, and consequences. Many of the recommendations I see in government management plans are both financially foolish and detrimental to your trees' health.

If you have timber that is harvestable in wet-weather conditions, make sure you plan well ahead of the sale—this means knowing the products you have and having your boundaries established and mapped. A quick inventory of the timber and some fresh paint on the boundaries and your stand will be ready for the bid market. Stumpage prices spike and subside rapidly, and if it takes too long to prepare your tract for sale, you will probably miss the wave.

If you plan on waiting for substantially better pine sawtimber prices before harvesting, find a comfortable chair because it will be a while. Pine owners need to come to terms with the reality that their value gains will come mostly from biological volume growth, not product price increases or premiums paid for quality for the foreseeable future.

The small-scale logger is quickly becoming a thing of the past, meaning low-volume stands are harder and harder to sell. Group low-volume stands with others on your property or work with adjoining landowners to combine sales to make them more attractive to buyers.

Be patient. Unless your tract is suited for wet-weather logging, accept that your cutting contract length will be at least two years. Most buyers are flush with timber to cut and not nearly as willing to fit in rush jobs.

Do not base your sale timing on housing starts and lumber price data—it may seem counterintuitive, but southern pine stumpage prices do not track strongly with those numbers.

If you are a timberland investor, you should focus on improving the appeal of your land. Invest some of your harvest revenues into road improvements, plantings, and understory and invasives control. Land prices continue to rise in the areas surrounding Charlotte, NC (my work area) and should continue to do so. A property with desirable accessibility and aesthetics is worth more and will sell more quickly than one lacking these characteristics. Buying a property that needs work is like buying a car or house that needs work—you expect a deal. The small investments you make to improve your land will pay for themselves in the long run. More on preparing and marketing your timberland here.

When selling timber, make the sale layout and terms as buyer-friendly and straightforward as possible. A proper sale invitation should have concise sale terms, timber volume data and statistics, quality maps (location, aerial, and topographic), sale area shapefiles (for the bidders' data logger/GPS), and a clearly delineated (on the ground with paint) sale area. Before the Great Recession, you could place almost any tract of timber on the bid market and get a fair number of competitive offers. Those days are over—it's a buyers' market, especially for pine-heavy sales. Buyers aren't as hungry and do not have the stomach for risk they once did. Fewer and fewer buyers are willing to invest their time negotiating and pricing tracts directly with landowners unless they are getting a deal. Most landowners lack the requisite skills and knowledge to put together an attractive sale. Hiring a private forestry consultant will yield higher bids and result in a better logging job.

I hope I'm wrong about the future of pine sawtimber pricing. Who knows, hurricanes, insects, disease, newly developed products, or fiber demand could eat into pine inventories and balance the sawtimber supply and demand. Regardless of what comes to pass, implementing the management strategies I've recommended will improve your future value and sales position. As always, feel free to contact me with any questions you may have.

Comments